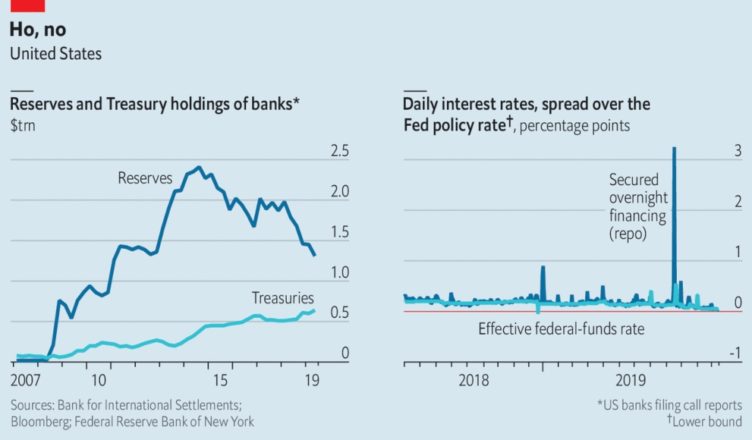

In September an often overlooked but vital part of the global financial system short-circuited. It’s called the overnight repurchase agreement, or “repo,” market, and when it seized up, the interest rate that institutional borrowers had to pay for very short-term loans went (briefly) through the roof.

In the aftermath, people in the market sought answers—to understand both what had gone wrong and the risk of it happening again. Many have turned to a Credit Suisse Group AG analyst named Zoltan Pozsar, who predicted the breakdown with almost eerie accuracy in an August research note.

Pozsar has some bad news: There’s more trouble ahead. Despite the Federal Reserve’s recent move to pump almost $500 billion into the repo market to prevent a yearend funding squeeze, deep-rooted problems remain.

The extent of those problems could become clear before the close of 2019, as banks scramble to get their books in order for regulators. “If the yearend is less of a problem because of the repo bazooka we got from the Fed, and if the message of my report played a part in getting that bazooka, then that’s a nice way to be proven wrong,” Pozsar says. “But now we’re getting into a point in the year when balance-sheet problems are going to flare up, and I think the system will get gummed up again.”

If he’s right, it means there’s something amiss in a more than $2 trillion market that lubricates the gears of finance. The repo market is where the cash-rich of the financial system lend to the cash-poor, with banks, money-market funds, hedge funds, broker-dealers, asset-managers, and others borrowing and lending to each other short-term. While borrowers in this system have plenty of longer-term assets, on a day-to-day basis they may not have the liquidity they need. Repo lets them borrow cash against those assets to tide them over.

In finance, a lack of liquidity “kills you quick,” says Perry Mehrling, a Boston University economics professor who co-authored a 2013 paper with Pozsar. “How do you not get killed by liquidity? By rolling it over. By saying, ‘I can’t make the payment today. I’ll make it tomorrow.’ That’s basically what overnight repo does.”

On Sept. 17, throughout Wall Street, fund managers were suddenly hurting for this short-term cash, and big banks seemed unwilling or unable to provide it. At the heart of Pozsar’s argument is the idea that two grand experiments—one in monetary policy, the other in regulation—have collided to make the repo market more prone to clogging up in this way.

The monetary experiment is quantitative easing. After the financial crisis, the Fed began stimulating the economy by buying bonds. The money it spent to do so added to the excess reserves held by banks. After years of QE, big banks became accustomed to always having cash to lend in the repo market—they were swimming in excess reserves.

But then the Fed began tapering off QE, buying fewer bonds and reducing the excess reserves in the system. There’s still a lot, but this is where the regulatory experiment comes in. To prevent a repeat of the 2008 crash, bank watchdogs have tightened rules in such a way that the biggest lenders feel they have to keep more reserves on hand. So falling reserves and banks’ desire to hold on to more began to pinch.

At the same time, other financial players were starting to rely more on the repo market. “There’s been a very sharp increase in the demand for funding in the last 12 months, in particular from levered investors such as hedge funds,” says Joseph Abate, money-market strategist at Barclays Plc. In September all these forces combined with a few other quirky events—such as corporations needing cash to settle quarterly tax bills—to create a brief systemwide shortage of ready cash.

Pozsar says another squeeze is likely. The potential results? Pain for hedge funds that use the repo market as a source of cheap money and a potential ripple effect on assets such as stocks and bonds as investors are forced to cut back on positions. His boldest prediction is that the Fed could push more liquidity into the system by buying longer-term Treasuries again. Pozsar says that would amount to a new round of QE.

In this case, the goal would be to keep things running smoothly, not to stimulate the economy. Some analysts say the central bank is already on top of the situation. “The Fed has been very proactive in addressing the liquidity concerns that emerged in September,” says Jerome Schneider, head of short-term bond portfolios at Pacific Investment Management Co. The issue, he says, “is not that there won’t be enough liquidity, but what the cost of that liquidity will be.”

Pozsar’s warnings get attention on Wall Street because he has a big-picture view of this complex market and can explain it well—at least to those fluent in the language of repoland. “I think he has every short-term interest-rate trader in the world on his speed dial,” Mehrling says. “He’s like a spider in the middle of the web, where he can gather this information and then try to make sense of it.”

Born in Hungary, Pozsar moved to the U.S. in 2002 and began his career at research company Economy.com. In 2008, shortly before the collapse of Lehman Brothers, he went to work at the Federal Reserve Bank of New York, where he became known for creating a map of the financial system that included repo and “shadow” banks outside of traditional lending. It’s so detailed that anyone viewing it on a computer has to zoom in seven or eight times to read any part of it. A poster version was pinned up in the New York Fed’s briefing room. Pozsar encouraged co-workers to stop by to review it, saying otherwise they’d be looking at only “10% of the picture.”

After a stint at the U.S. Treasury Department, he landed at Credit Suisse in 2015, where he began writing research notes about the mechanics of the Fed’s coming interest-rate hike. Pozsar has an MBA but not an economics degree, and his analytical approach differs from that of other bank interest-rate strategists. He focuses more on the human behavior inside banks. “Finance is anthropological,” he says. He thinks it’s important to understand that every bank has a different business model, and how that shapes people’s decisions to lend—or not. Even at a time when the numbers say they have plenty of money.

Bloomberg. Cuándo se impusieron las medidas de cuarentena y confinamiento por países